With memory prices towering sky-high as chips are getting fast-sold to the highest bidders, evidently, the large AI companies, global shipments of entry-level phones have dipped ever lower. According to manufacturers, storage hardware in low-end phones now takes up about 60% of the Bill of Materials (BoM). That’s incredible, and also, unconvincingly limiting to the budget phone market in meeting the demands that have hardly fallen.

Even a year ago, amid concerns that mid-range smartphones would lose consumer favour and hence production volume, analysts still felt confident about a consistent budget-friendly segment, which had been around 41% to 45% for half the decade. Afterwards, the unsettling condition, resulting from multiple interplaying factors, including price hike, shipment contraction, and realignment of regional markets, cut that confidence thinner.

Unprecedented Prices

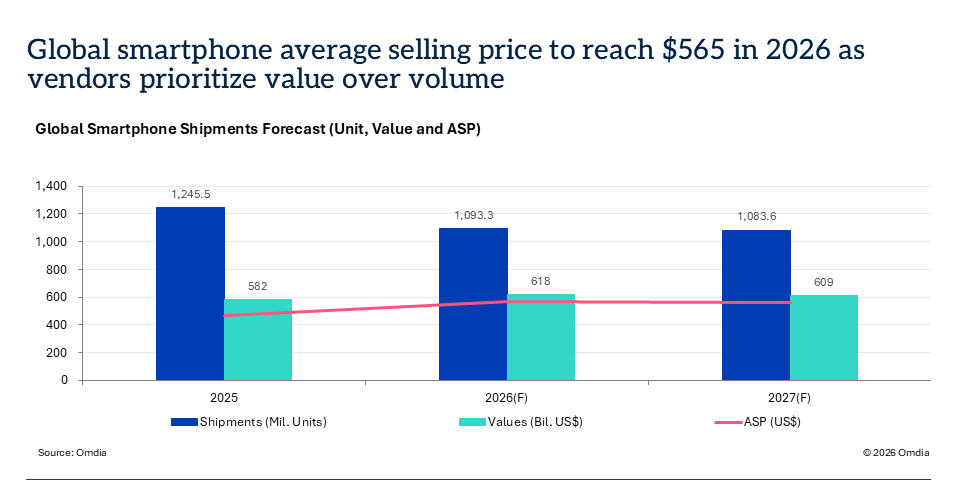

The early quarter of 2026 turned the tables, unnerving both consumers and analysts. In June this year, a global tech research group, Omdia, forecast a layout shift that’s to move the global smartphone average selling price (ASP) from $467 to $565 within just a year. An astounding 21% year-over-year increase. Through a zoomed-in lens, this rise appears steeper in the under-$400 device group and angles down gradually as phones become pricier.

Moreover, Dynamic Random-Access Memory (DRAM) and Flash Memory (NAND), two components used as data keeps in phones, whether for temporary retrieval or permanent storage, are seeing crazy outbursts, both in demand and making. However, their largest share is shipped directly off the factory to AI labs around the world. Most of it goes into developing High-Bandwidth Memory (HBM) in trainable intelligent modules.

With this, DRAM and NAND’s rate has hit an all-time high, by over 80% quarter-on-quarter (QoQ). For phone makers, the disruption from material scarcity and added expense is nothing less than a dilemma that must be managed without trimming down on the annual ROI target volume. Rationally, keeping low-priced phone production in check seems like a choice with zero alternatives.

Minimum Shipments

This is happening just so. Fewer low-end devices are coming to retailers. For instance, the number of global smartphone shipments has already tumbled and is reflecting a 12.2% year-on-year reduction, about 152 million units not coming out of the factory in 2026.

The gap from plummeting deliveries is being realized by a swelling marketing value, to be exact, 6.1% within the same timeline. For people, it means no more lucrative phone deals to swap your old ones, unless someone spends over $600 or so. As well, the extra money won’t let them get into mid-range showcases; they will be buying the same low-end models.

Regional Impacts

Statistically, by far, much of Asia, Africa, and Latin America have been the largest distribution zones for budget phones. The recent ecological change in the industry has seemingly nudged that demand curve downward. If the situation drags on long enough, and it likely will, as per opinions from analysts, people’s buying habits may evolve.

Save Apple, all new-gen handsets have been repriced to some extent, to cope with high material costs. Premium phones are observing an upturn as the wisest choice for the money right now.

Budget Phone Market Future Projection

Prior research hinted at a year-long stagnation in the budget phone market. More recent data only stretches the duration further to the early quarter of 2028. Market experts are hopeful that an alternative innovation may take place and replace the need for traditional memory chips. Even without such a thing happening, the hardware price will revert to normal eventually. It may take till AI investment slows down or simply memories hit the sufficient quota. A lot will change for brands and users, strategically and habitually, before that.

No comments yet. Be the first to comment.